What Happens to Your Money When You Die in Canada?

What happens to your money when you die in Canada? When someone passes away, the government may tax their assets through rules like deemed disposition and income inclusion.

| Important: This article is for learning only. It is not financial, tax, or legal advice. Every person’s situation is different. Please talk to a qualified tax expert, estate lawyer, or financial advisor before making any decisions. Horizon Growth only works with CRA-compliant strategies. |

Most people who come to Canada are surprised to hear this:

Canada does not have an estate tax. There is no death tax. There is no tax on what you leave your children.

That sounds like great news. And in some ways, it is.

But here is the part that most people do not know — and it is important:

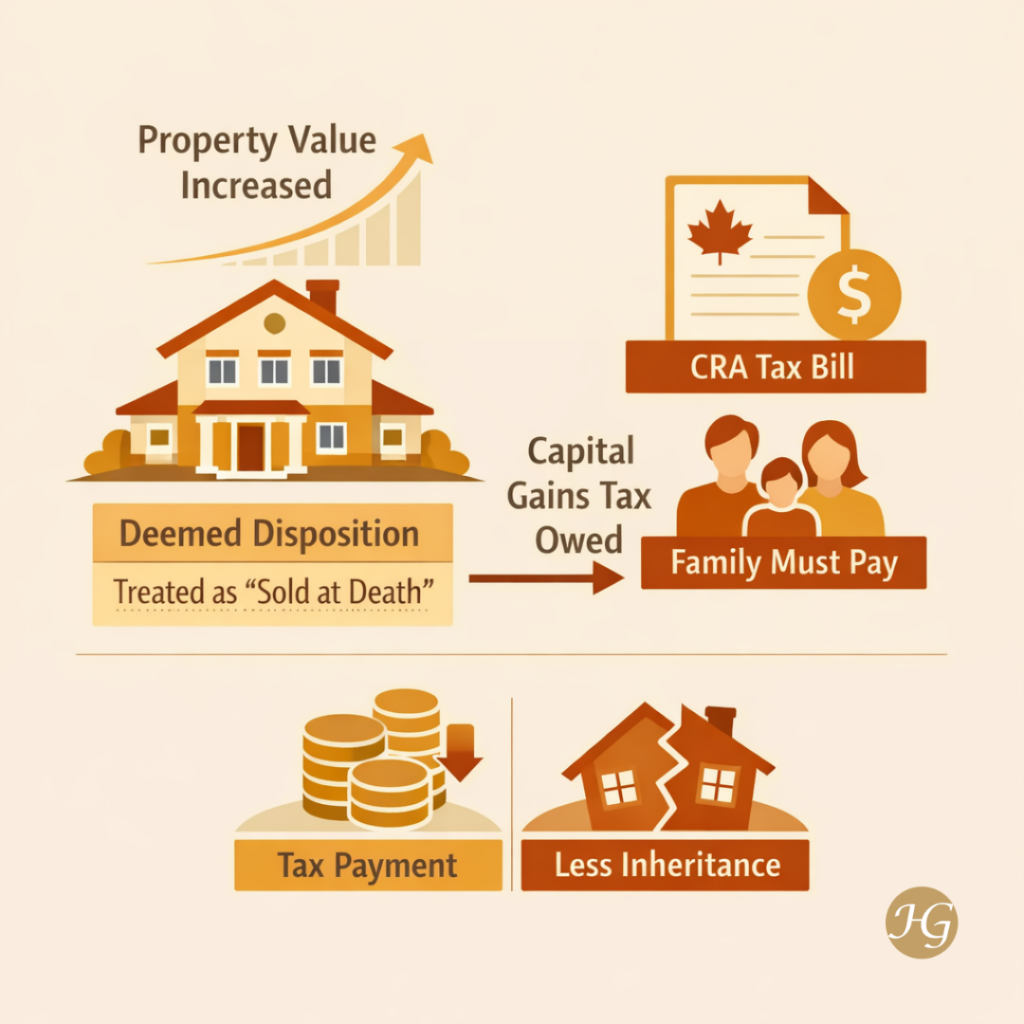

The day you die in Canada, the government acts as if you sold everything you owned — your home, your investments, your business — all on that one day. The profit from that sale? The government wants its share.

This is called deemed disposition. It is one of the biggest surprises families face when someone passes away. And the families who are hit hardest are often the ones who worked the hardest — people who bought property, built businesses, and saved carefully for decades.

This article explains what deemed disposition is, how it works, and what questions you should ask a professional. We will use simple, clear language — no confusing terms without explanation.

What Is Deemed Disposition?

“Deemed disposition” is a tax rule in Canada.

The word “deemed” means something is treated as if it happened — even if it did not.

So what does this mean?

When you pass away, the government treats it as if you sold everything you own on that day.

You did not actually sell anything.

But for tax purposes, it is treated that way.

Why Does Canada Have This Rule?

Canada taxes the profit people make when they sell assets like property and investments.

If this tax was never collected at death, large amounts of wealth could pass from one generation to the next without ever being taxed.

The deemed disposition rule makes sure the tax is paid — even if nothing is sold.

What Does This Rule Apply To?

This rule applies to many types of assets, including:

- Stocks and investments (shares, mutual funds, bonds)

- Rental properties (homes you rent out)

- Cottages or vacation homes

- Shares in a family business or private company

How Is the Tax Calculated?

In simple terms, the tax comes from your profit.

This profit is the difference between:

- what you originally paid

- and what the asset is worth when you die

As a result, this difference becomes a capital gain.

| Simple example: Your parents bought a rental house for $200,000. When they pass away, it is worth $700,000. The profit is $500,000. The government treats that $500,000 as income on their final tax return — even though the house was never sold. |

How Much Tax Could This Be?

In Canada, you do not pay tax on the full profit.

Instead, only a portion of the gain becomes taxable income. This portion is called the inclusion rate.

Currently, the inclusion rate is 50%.

So, for example:

- A $500,000 gain becomes $250,000 of taxable income

However, this amount is added to your total income for that year.

As a result, it can push the estate into a higher tax bracket. In many provinces, combined tax rates can reach 46% to 54%.

Why this matters

Because everything happens in one year.

That can push the estate into the highest tax bracket.

And the tax bill must usually be paid before anything is passed on to the family.

| Important Note In 2024, the government proposed increasing the inclusion rate to 66.67%. However, in March 2025, Prime Minister Mark Carney cancelled this plan. As a result, the rate remains at 50% — for now. That said, the inclusion rate has changed several times since 1972 and has been as high as 75% in the past. Therefore, it is important to understand that these rules can change again in the future. |

Are There Any Exceptions?

Yes — and these exceptions matter.

However, they depend heavily on your personal situation. That is why professional guidance plays an important role.

A Hidden Risk Many Families Face

Many families do not realize this risk.

The tax bill often comes due quickly. However, most estates hold value in assets rather than cash.

Because of this, a challenge can arise.

Estates are often made up of:

- Property

- Businesses

- Long-term investments

As a result, families may need to sell assets — sometimes quickly — just to cover the tax bill.

In some cases, this means letting go of assets they had hoped to keep.

For many families, this becomes one of the most difficult and unexpected parts of estate planning.

However, with proper planning, this situation can often be avoided.

Leaving Assets to Your Spouse

If you leave assets to your spouse or common-law partner, the tax does not apply right away.

We call this strategy a spousal rollover.

Instead of using today’s value, the system transfers the assets at their original cost.

As a result, the tax is delayed.

However, it does not disappear.

The tax will still apply later:

- when your spouse sells the asset

- or when your spouse passes away

Your Main Home (Principal Residence Exemption)

Your primary home usually qualifies for the Principal Residence Exemption.

Because of this, no tax applies when you pass away.

However, there are limits.

The exemption:

- applies to only one home per family at a time

- does not cover additional properties

This includes:

- Rental properties

- Cottages

- Vacation homes

Therefore, if you own more than one property, this becomes an important planning area.

Farm or Fishing Property

Special rules apply to farm and fishing businesses.

In some cases, these rules can reduce or delay tax when you transfer these assets to children or grandchildren.

However, these rules can become complex.

Therefore, professional advice is strongly recommended.

Not All Assets Are Taxed the Same Way

So far, we have talked about assets like property and investments.

These are taxed through capital gains when someone passes away.

However, not all assets follow the same rules.

Some accounts are taxed differently — and in many cases, more heavily.

One of the most important examples is the RRSP.

What About RRSPs?

Many Canadians use an RRSP (Registered Retirement Savings Plan) to save for retirement.

While you are alive:

- Contributions reduce your taxable income

- Investments grow without immediate tax

However, things change at death.

The full RRSP value becomes part of your income for that year

Not as a capital gain — but as regular income.

Because of this, it is taxed at higher rates.

| Example: If your RRSP holds $400,000: A large portion — possibly $180,000 to $210,000 or more — may go to taxes, depending on your province. |

Important Exception

If you transfer the RRSP to a spouse:

- The tax is deferred

- The timing shifts to the future

A Simple Way to Think About It

An RRSP is not tax-free.

Instead, it delays tax.

You received a benefit earlier.

Later, the tax becomes due — often at death.

What Is a Clearance Certificate?

When someone passes away, an executor manages the estate.

Before distributing any assets, the executor should request a Clearance Certificate from the CRA.

This document confirms that all taxes have been paid.

⚠ Many executors do not know about this rule. They want to help the family quickly and start sharing the estate right away. But sharing too soon can create serious personal risk. Always speak to a tax professional or estate lawyer before distributing an estate.

Why This Matters Right Now

Over the past 20 to 30 years, property values have increased significantly, investment portfolios have grown, and many businesses have become more valuable.

As a result, the “paper profit” is larger than ever.

And with that, the potential tax has also increased.

Even families who do not consider themselves wealthy can face large tax bills, difficult decisions, and unexpected stress.

Tax will affect your estate. That is almost certain. The only question is whether your family will be ready for it — or whether it will come as a shock when it is too late to plan.

Questions to Ask a Professional

You do not need to solve everything today.

However, you can start by asking better questions:

- Do you know how much unrealized profit you have today?

- Does your estate plan account for tax — not just distribution?

- Have you reviewed what happens to your assets at death?

- Does your spouse understand the future tax impact?

- How much of your RRSP will go to taxes?

- When did you last update your will?

✓ These questions do not need to be answered today. But they are much better asked now — while there is still time to plan — than discovered by your family after you are gone.

A Final Word

Many immigrants come to Canada and work incredibly hard.

Over time, they buy homes, build businesses, and learn to save with discipline. Along the way, they make sacrifices — all so their children and grandchildren can have a better life.

Understanding how Canada’s tax system works — including what happens to your money when you die — is one of the most important gifts you can give your family.

Not because it replaces a lawyer or a tax expert. It does not.

But because it helps you ask the right questions, at the right time, with the right people.

At Horizon Growth, we believe financial education belongs to everyone — not just the wealthy, not just accountants, and not just those who were born here.

Instead, every hard-working Canadian deserves to understand the system they are building their future inside.

| Disclaimer and Sources This article is for educational purposes only and does not constitute financial, tax, legal, or estate planning advice. Tax rules in Canada are complex and may change, and every situation is different. Please consult a qualified tax professional, estate lawyer, or licensed financial advisor before making decisions. Esther Sande holds the Real Wealth Manager (RWM™) designation from Knowledge Bureau. This is an educational designation and does not authorize regulated financial advice or product recommendations. Sources: Explanation for Deemed Disposition in Canada: Capital Gains and Inclusion Rates |

About the Author

Esther Sande is the founder of Horizon Growth and a Financial Success Mentor who helps individuals and families understand how to grow, protect, and pass on their wealth with clarity and intention.

She holds the Real Wealth Manager (RWM™) designation from Knowledge Bureau, a program that focuses on tax-efficient wealth building, estate planning, and long-term financial strategy.

Esther is passionate about making financial concepts simple and accessible — especially for immigrants, professionals, and business owners who are working hard to build a better future, but want to understand the system they are building within.